Compare the standard HP filter with the Modified HP filter for a single series. Provides summary statistics for both methods including cycle properties.

Usage

mhp_compare(x, frequency = c("quarterly", "annual"), max_lambda = 100000L)Value

A data.table with comparison statistics for both methods:

- method

"HP" or "Modified HP"

- lambda

Smoothing parameter used

- cycle_sd

Standard deviation of cyclical component

- cycle_mean

Mean of cyclical component

- ar1

First-order autocorrelation of cyclical component

- cycle_range

Range of cyclical component (max - min)

- gcv

GCV value (NA for standard HP)

Details

The comparison includes: 1. Standard HP filter with fixed lambda (1600 for quarterly, 100 for annual) 2. Modified HP filter with GCV-optimized lambda

Statistics calculated on the cyclical component help assess filter performance: - Lower cycle SD suggests smoother trend - AR(1) near 0 suggests successful cycle extraction - Near-zero mean suggests proper centering

Examples

# Example 1: Quarterly GDP-like series

set.seed(789)

n <- 100

gdp <- cumsum(rnorm(n, mean = 0.7, sd = 0.5)) + 2 * cos(2 * pi * (1:n) / 32)

comparison <- mhp_compare(gdp, frequency = "quarterly", max_lambda = 10000)

print(comparison)

#> method lambda cycle_sd cycle_mean ar1 cycle_range gcv

#> <char> <num> <num> <num> <num> <num> <num>

#> 1: HP 1600 0.9492746 2.372129e-12 0.8547305 3.882929 NA

#> 2: Modified HP 206 0.5323633 -3.261835e-13 0.6231910 2.408114 0.552981

# Example 2: Annual series

set.seed(101)

n_annual <- 50

annual_series <- cumsum(rnorm(n_annual, mean = 2.0, sd = 1.0)) +

3 * sin(2 * pi * (1:n_annual) / 10)

annual_comparison <- mhp_compare(annual_series, frequency = "annual", max_lambda = 5000)

print(annual_comparison)

#> method lambda cycle_sd cycle_mean ar1 cycle_range gcv

#> <char> <num> <num> <num> <num> <num> <num>

#> 1: HP 100 2.130999 -2.198952e-13 0.7444730 7.759845 NA

#> 2: Modified HP 956 2.441077 2.926424e-12 0.7834235 9.780873 6.450526

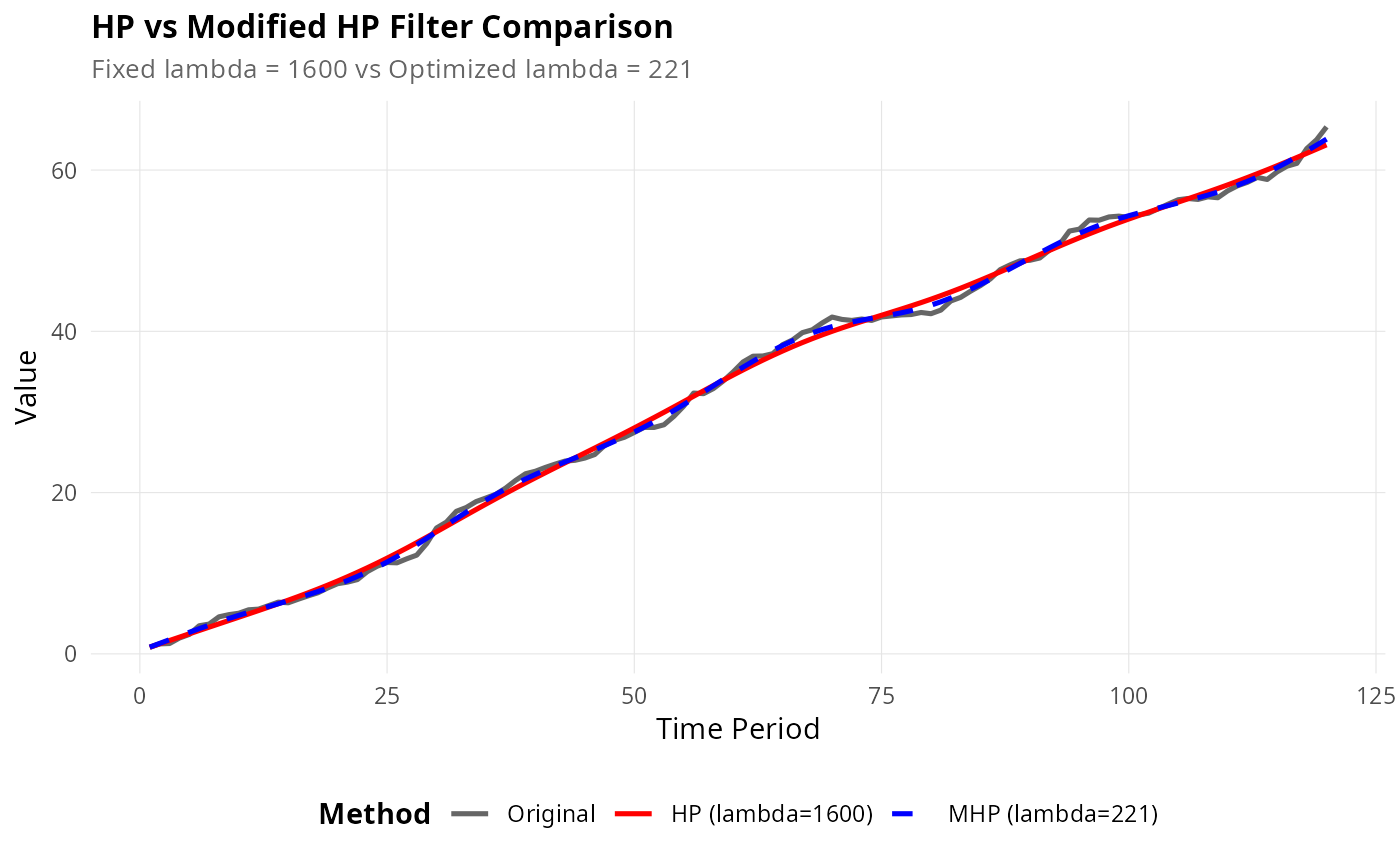

# Example 3: Visual comparison

set.seed(2023)

test_series <- cumsum(rnorm(120, mean = 0.5, sd = 0.4)) +

runif(1, 1, 3) * sin(2 * pi * (1:120) / 30)

comp_result <- mhp_compare(test_series, frequency = "quarterly", max_lambda = 20000)

if (require(ggplot2)) {

# Create visualization

hp_result <- hp_filter(test_series, lambda = 1600, as_dt = FALSE)

mhp_result <- mhp_filter(test_series, max_lambda = 20000, as_dt = FALSE)

plot_comparison(test_series, frequency = "quarterly", max_lambda = 20000)

}